By ROBERT H. FRANK

Published: October 16, 2010

PEOPLE often remember the past with exaggerated fondness. Sometimes, however, important aspects of life really were better in the old days.

David G. Klein

During the three decades after World War II, for example, incomes in the United States rose rapidly and at about the same rate — almost 3 percent a year — for people at all income levels. America had an economically vibrant middle class. Roads and bridges were well maintained, and impressive new infrastructure was being built. People were optimistic.

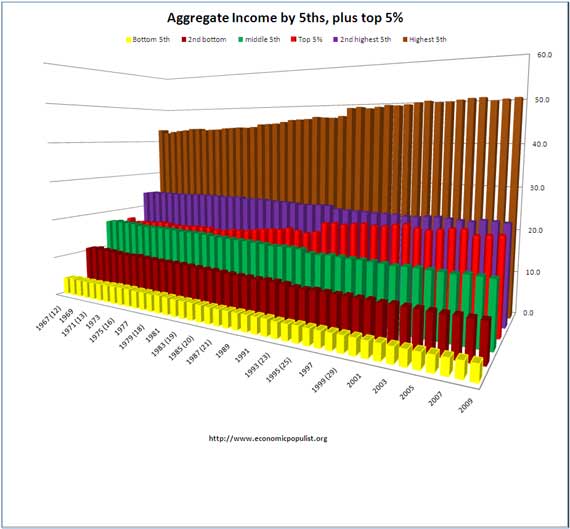

By contrast, during the last three decades the economy has grown much more slowly, and our infrastructure has fallen into grave disrepair. Most troubling, all significant income growth has been concentrated at the top of the scale. The share of total income going to the top 1 percent of earners, which stood at 8.9 percent in 1976, rose to 23.5 percent by 2007, but during the same period, the average inflation-adjusted hourly wage declined by more than 7 percent.

Yet many economists are reluctant to confront rising income inequality directly, saying that whether this trend is good or bad requires a value judgment that is best left to philosophers. But that disclaimer rings hollow. Economics, after all, was founded by moral philosophers, and links between the disciplines remain strong. So economists are well positioned to address this question, and the answer is very clear.

Adam Smith, the father of modern economics, was a professor of moral philosophy at the University of Glasgow. His first book, “A Theory of Moral Sentiments,” was published more than 25 years before his celebrated “Wealth of Nations,” which was itself peppered with trenchant moral analysis.

Some moral philosophers address inequality by invoking principles of justice and fairness. But because they have been unable to forge broad agreement about what these abstract principles mean in practice, they’ve made little progress. The more pragmatic cost-benefit approach favored by Smith has proved more fruitful, for it turns out that rising inequality has created enormous losses and few gains, even for its ostensible beneficiaries.

Recent research on psychological well-being has taught us that beyond a certain point, across-the-board spending increases often do little more than raise the bar for what is considered enough. A C.E.O. may think he needs a 30,000-square-foot mansion, for example, just because each of his peers has one. Although they might all be just as happy in more modest dwellings, few would be willing to downsize on their own.

People do not exist in a social vacuum. Community norms define clear expectations about what people should spend on interview suits and birthday parties. Rising inequality has thus spawned a multitude of “expenditure cascades,” whose first step is increased spending by top earners.

The rich have been spending more simply because they have so much extra money. Their spending shifts the frame of reference that shapes the demands of those just below them, who travel in overlapping social circles. So this second group, too, spends more, which shifts the frame of reference for the group just below it, and so on, all the way down the income ladder. These cascades have made it substantially more expensive for middle-class families to achieve basic financial goals.

In a recent working paper based on census data for the 100 most populous counties in the United States, Adam Seth Levine (a postdoctoral researcher in political science at Vanderbilt University), Oege Dijk (an economics Ph.D. student at the European University Institute) and I found that the counties where income inequality grew fastest also showed the biggest increases in symptoms of financial distress.

For example, even after controlling for other factors, these counties had the largest increases in bankruptcy filings.

Divorce rates are another reliable indicator of financial distress, as marriage counselors report that a high proportion of couples they see are experiencing significant financial problems. The counties with the biggest increases in inequality also reported the largest increases in divorce rates.

Another footprint of financial distress is long commute times, because families who are short on cash often try to make ends meet by moving to where housing is cheaper — in many cases, farther from work. The counties where long commute times had grown the most were again those with the largest increases in inequality.

The middle-class squeeze has also reduced voters’ willingness to support even basic public services. Rich and poor alike endure crumbling roads, weak bridges, an unreliable rail system, and cargo containers that enter our ports without scrutiny. And many Americans live in the shadow of poorly maintained dams that could collapse at any moment.

ECONOMISTS who say we should relegate questions about inequality to philosophers often advocate policies, like tax cuts for the wealthy, that increase inequality substantially. That greater inequality causes real harm is beyond doubt.

But are there offsetting benefits?

There is no persuasive evidence that greater inequality bolsters economic growth or enhances anyone’s well-being. Yes, the rich can now buy bigger mansions and host more expensive parties. But this appears to have made them no happier. And in our winner-take-all economy, one effect of the growing inequality has been to lure our most talented graduates to the largely unproductive chase for financial bonanzas on Wall Street.

In short, the economist’s cost-benefit approach — itself long an important arrow in the moral philosopher’s quiver — has much to say about the effects of rising inequality. We need not reach agreement on all philosophical principles of fairness to recognize that it has imposed considerable harm across the income scale without generating significant offsetting benefits.

No one dares to argue that rising inequality is required in the name of fairness. So maybe we should just agree that it’s a bad thing — and try to do something about it.

Robert H. Frank is an economics professor at the Johnson Graduate School of Management at Cornell University.

No comments:

Post a Comment